|

CREDICORP LTD.

(Registrant)

|

|||

|

By:

|

/s/ José Luis Muñoz

|

||

|

José Luis Muñoz

|

|||

|

Authorized Representative

|

|||

Exhibit 99.1

| CREDICORP LTD. AND SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2025, AND 2024 |

||

CREDICORP LTD. AND SUBSIDIARIES

CONSOLIDATED FINANCIAL STATEMENTS

AS OF DECEMBER 31, 2025, AND 2024

| CONTENTS | Pages |

| Independent auditor’s report | 1 - 8 |

| Consolidated statement of financial position | 9 |

| Consolidated statement of income | 10 - 11 |

| Consolidated statement of comprehensive income | 12 |

| Consolidated statement of changes in equity | 13 -14 |

| Consolidated statement of cash flows | 15 - 18 |

| Notes to the consolidated financial statements | 19 - 178 |

| S/, Sol | = Sol |

| US$ | = U.S. Dollar |

| Bs | = Boliviano |

| $ | = Colombian Peso |

| ¥, Yen | = Japanese Yen |

| |

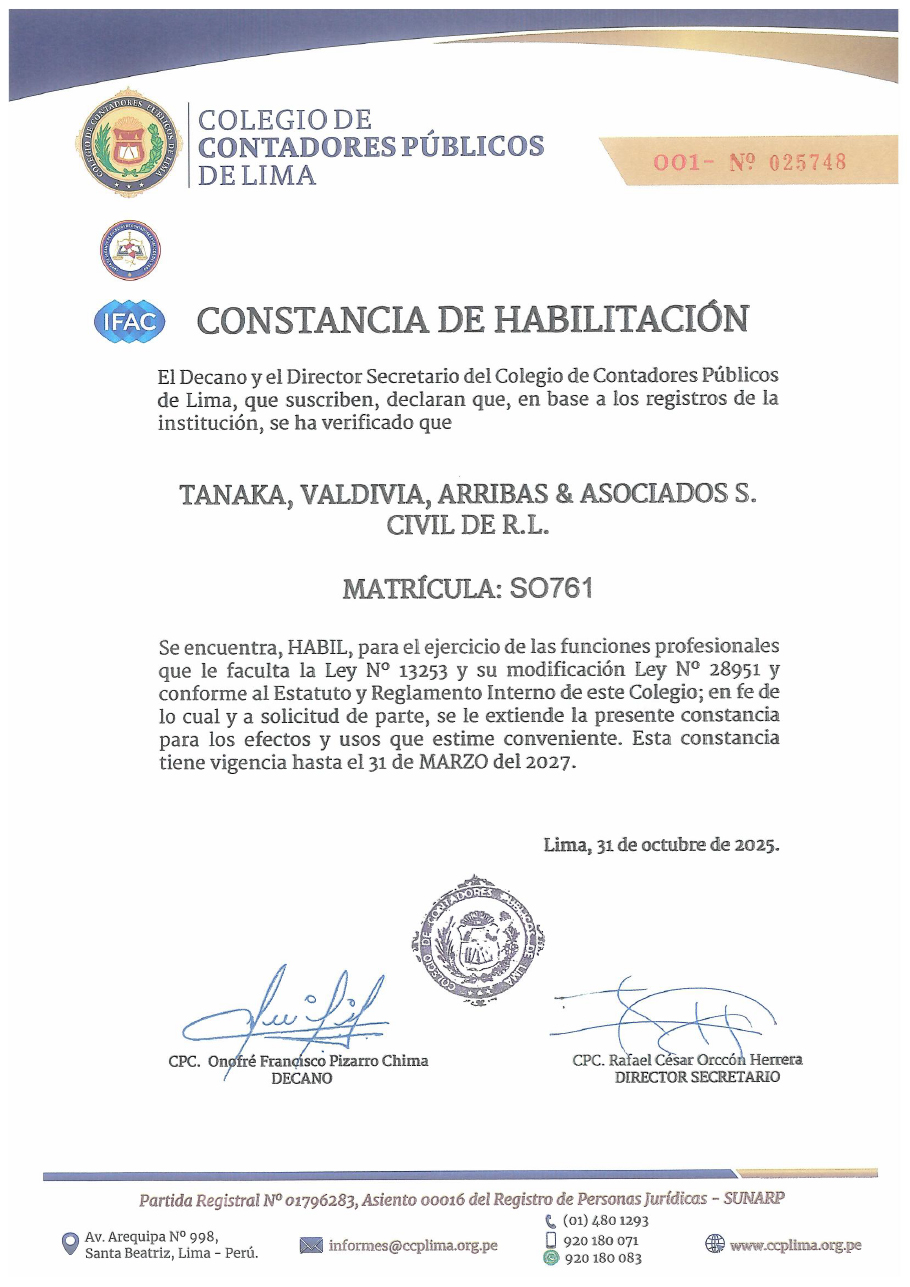

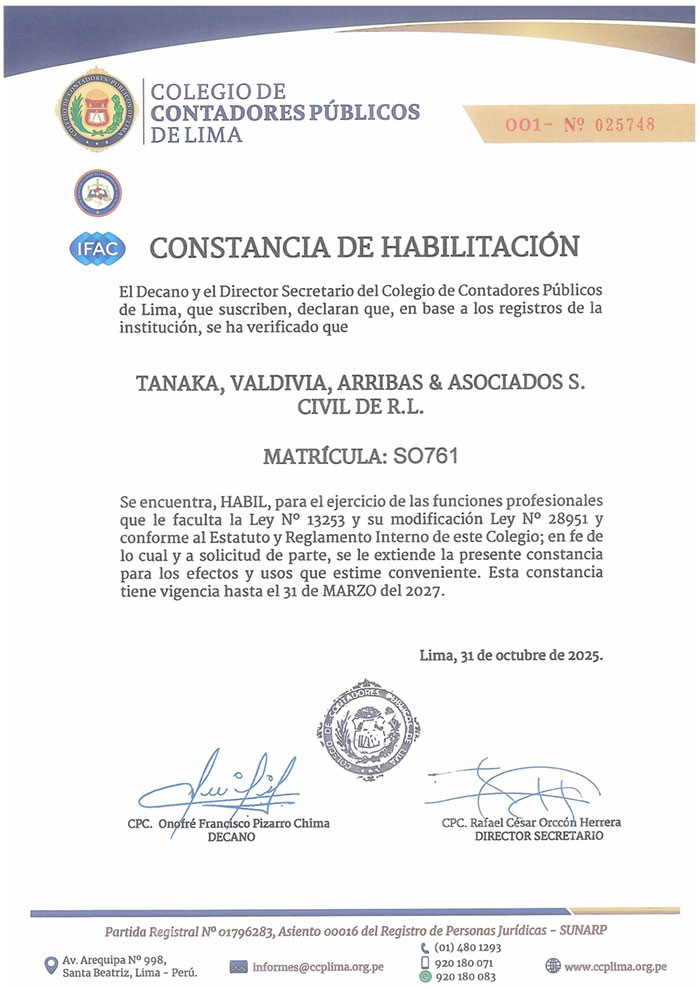

Tanaka, Valdivia, Arribas & Asociados Sociedad Civil de R. L |

Independent auditor’s report

To the Shareholders and Directors of Credicorp Ltd.

Report on the audit of the consolidated financial statements

Opinion

We have audited the consolidated financial statements of Credicorp Ltd. and its subsidiaries (the Group), which comprise the consolidated statement of financial position as at December 31, 2025, and the consolidated statements of income, comprehensive income, changes in equity and cash flows for the year then ended, and notes to the consolidated financial statements, including material accounting policy information.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Group as at December 31, 2025, and its consolidated financial performance and its consolidated cash flows for the year then ended in accordance with IFRS Accounting Standards.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs) approved for application in Peru by the Board of Deans of Associations of Public Accountants of Peru. Our responsibilities under those standards are further described in the Auditor's responsibilities for the audit of the consolidated financial statements section of our report. We are independent of the Group in accordance with the International Ethics Standards Board for Accountants’ International Code of Ethics for Professional Accountants (including International Independence Standards) (IESBA Code), as applicable to audits of financial statements of public interest entities, together with the ethical requirements that are relevant to audits of the consolidated financial statements of public interest entities in Peru. We have also fulfilled our other ethical responsibilities in accordance with these requirements and the IESBA Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

| Lima Av. Víctor Andrés Belaunde 171, San Isidro |

Lima II Av. Jorge Basadre 330, San Isidro |

Lima III Av. Jorge Basadre 350, San Isidro |

Arequipa piso 13, Torre Sur, |

Trujillo Av. El Golf 591, Víctor Larco Herrera, Sede Miguel Ángel Quijano Doig, La Libertad |

Chiclayo (satélite) Lambayeque |

Cusco (satélite) Urb. Santa Mónica, |

|||||||

Inscrita en la partida 11396556 del Registro de Personas Jurídicas de Lima y Callao

Miembro de Ernst & Young Global

Independent auditor’s report (continue)

Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. For each matter below, our description of how our audit addressed the matter is provided in that context.

We have fulfilled the responsibilities described in the Auditor’s responsibilities for the audit of the consolidated financial statements section of our report, including in relation to these matters. Accordingly, our audit included the performance of procedures designed to respond to our assessment of the risks of material misstatement of the consolidated financial statements. The results of our audit procedures, including the procedures performed to address the matters below, provide the basis for our audit opinion on the accompanying consolidated financial statements.

| Key audit matter | How our audit addressed the key audit matter | ||

| Information Technology (IT) environment | |||

|

The Group's information technology (IT) environment consists of an infrastructure of a large number of key systems for the processing of its operations, accounting records and preparation of its consolidated financial statements. In addition, the Group's Management has designed a series of automatic controls, interfaces between the systems and executed calculations of the applications; with the aim of ensuring the completeness and accuracy of accounting records and accurate financial reports, thus mitigating the potential risk of fraud or error.

For the above reasons, we consider the information technology environment to be a key matter, given that the Group depends on the efficient and continuous operation of IT applications as well as their automatic controls, so there is a risk that breaches in the IT control environment may result in accounting records being materially misstated. |

With the support of our Information Technology (IT) professionals, our audit efforts focused on the key systems related to the processing of operations, accounting records and preparation of the Group's consolidated financial statements, for which we perform the following procedures:

|

||

| - | Evaluation of the Group's IT governance framework. | ||

| - | Understanding of the control environment and identification of risks of IT processes. | ||

| - | Testing key controls over application and data access management, program changes and application development and IT operations. | ||

| - | Testing of the design and operational effectiveness of the key automatic controls identified in the various relevant processes of the Group. | ||

| - | Testing of the design and operational effectiveness of applicable compensation controls. | ||

Independent auditor’s report (continue)

| Key audit matter | How our audit addressed the key audit matter |

| Expected credit loss on the loan portfolio | |

|

At December 31, 2025, the allowance for loan losses was S/8,042 million, as disclosed in note 7 to the consolidated financial statements. As more fully disclosed in Note 3(i) and 30.1 to the consolidated financial statements, the allowance for loan losses was calculated using an expected credit loss (ECL) model. The ECL model utilizes the probability of default (PD) as a key assumption.

Auditing the allowance for loan losses was complex and required the application of significant auditor effort in evaluating management’s calculation due to the inherent complexity related to the PD assumption, including the forward-looking forecasts across multiple economic scenarios and their associated probability weighting. The ECL is a significant estimate for which variations in model methodology, assumptions and judgments could have a material effect on the measurement of the allowance for loan losses.

|

We obtained an understanding, evaluated the design, and tested the operating effectiveness of management’s controls over the calculation of the allowance for loan losses. The controls we tested related, among others, to the significant assumptions described above, which included controls over the calculation of the PD, including the data inputs used and the governance and oversight controls over the review of the overall ECL model.

Our audit procedures, in which we involved professionals with specialized skills and knowledge to assist in evaluating the audit evidence obtained, included, among others, assessing whether the methodology and assumptions used to estimate the ECL were consistent with the requirements of IFRS 9, Financial Instruments. We also performed an independent recalculation of the allowance for loan losses for a sample of loan portfolio, focusing on the PD assumption due to its relevance within the ECL measurement and assessed the reasonableness of certain forward-looking assumptions used in the calculation of the PD by analyzing publicly available information from third-party sources. We also assessed the adequacy of the related disclosures included in the consolidated financial statements.

|

Independent auditor’s report (continue)

| Key audit matter | How our audit addressed the key audit matter |

| Valuation of the liability for life insurance contracts under the general measurement model | |

|

At December 31, 2025, the liability for life insurance contracts under the general measurement model was S/10,507 million, as disclosed in note 8 to the consolidated financial statements. Notes 3(e) and 30.9 also provide disclosures in respect of the foregoing. The determination of the liability for life insurance contracts under the general measurement model is calculated as the sum of cash flow projections related to each portfolio of insurance contracts considering their probability of occurrence and includes cash flow projections that are within the limit of each contract in the portfolio. Cash flow projections are computed based on current mortality tables and current discount interest rates as key assumptions.

Auditing the liability for life insurance contracts under the general measurement model was complex and required the application of significant auditor judgment due to the complexity of the actuarial models, the selection and use of judgmental assumptions and the interrelationship of these variables in measuring the liability. Changes in these assumptions, particularly the discount interest rate, could have a material effect on the liability for life insurance contracts under the general measurement model.

|

We obtained an understanding, evaluated the design, and tested the operating effectiveness of management’s controls, related to the liability for life insurance contracts under the general measurement model. The controls we tested related to, among others, the governance and oversight controls over the review of the actuarial models, the related assumptions and data inputs used.

Our audit procedures, in which we involved our actuarial specialists to assist in evaluating the audit evidence obtained, included, among others, the evaluation of the methodology, actuarial models and assumptions used by the Group to measure life insurance contract liabilities in accordance with IFRS 17, Insurance Contracts. We also tested the completeness and accuracy of the underlying data used in the measurement of the liability for life insurance contracts. With the support of our actuarial specialists, we performed an independent recalculation of the liability for life insurance contracts under the general measurement model and evaluated the discount interest rate used for a sample of contracts. We also assessed the adequacy of the related disclosures included in the consolidated financial statements.

|

Independent auditor’s report (continue)

| Key audit matter | How our audit addressed the key audit matter |

| Recognition of an asset related to a dispute with the tax authority | |

|

At December 31, 2025, the Group recognized an asset of S/ 1,577 million derived from a payment made in connection with a dispute with the Peruvian tax authority regarding income tax withholding on payments to a non-domiciled entity in 2018 and 2019, as disclosed in notes 12(a) and 31(ii) to the consolidated financial statements. The related dispute gives rise to an uncertain tax position due to the uncertainty regarding the applicability of Peruvian income tax laws to transactions with non-domiciled entities in Peru. The Group used significant judgement to determine, based on the technical merits, whether it was more likely than not that its tax position would prevail when determining the amount recognized.

Auditing the estimation of the outcome and measurement of the uncertain tax position from the payment made to the tax authority and the related recoverability of the asset, before the uncertain tax treatment is resolved, requires a high degree of auditor judgment and significant audit effort due to the complexity and judgment used by the Group in the assessment. |

We obtained an understanding, evaluated the design, and tested the operating effectiveness of management’s controls over the process for recognizing an asset related to a dispute with the Peruvian tax authority, as well as the process for evaluating the uncertain tax position.

Our audit procedures included, among others, evaluating the assumptions used by the Group to assess its uncertain tax positions based on relevant Peruvian income tax laws, including the inspection of the Group’s external counsel’s analysis of these matters and evaluated the completeness and accuracy of the data used to determine the amount recognized and tested the accuracy of such calculations. In addition, we involved our tax subject matter professionals to assess the technical merits of the Group’s tax position and evaluate the application of relevant tax law in assessing the recoverability of payment made. We also assessed the adequacy of the related disclosures in the consolidated financial statements. |

Other information included in the Group's 2025 Annual Report

Other information consists of the information included in the Annual Report, other than the consolidated financial statements and our auditor’s report thereon. Management is responsible for the other information.

Our opinion on the consolidated financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

Independent auditor’s report (continue)

In connection with our audit of the consolidated financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of management and those charged with Group’s governance for the consolidated financial statements

Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with IFRS Accounting Standards, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the Group's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

Those charged with Group’s governance are responsible for overseeing the Group's financial reporting process.

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

Independent auditor’s report (continue)

As part of an audit in accordance with ISAs approved for application in Peru, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

| - | Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. |

| - | Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group's internal control. |

| - | Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management. |

| - | Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group to cease to continue as a going concern. |

| - | Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation. |

| - | Plan and perform the group audit to obtain sufficient appropriate audit evidence regarding the financial information of the entities or business units within the group as a basis for forming an opinion on the consolidated financial statements. We are responsible for the direction, supervision and review of the audit work performed for the purposes of the group audit. We remain solely responsible for our audit opinion. |

We communicate with those charged with Group's governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Independent auditor’s report (continue)

We also provide those charged with Group's governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, actions taken to eliminate threats or safeguards applied.

From the matters communicated with those charged with Group's governance, we determine those matters that were of most significance in the audit of the consolidated financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

Lima, Peru

February 26, 2026

Endorsed by:

|

|

Victor Tanaka

Partner-in-Charge

C.P.C.C. Registration No. 25613

CREDICORP LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

AS OF DECEMBER 31, 2025 AND 2024

| Note | 2025 | 2024 | ||||||||

| S/(000) | S/(000) | |||||||||

| Assets | ||||||||||

| Cash and due from banks: | ||||||||||

| Non-interest-bearing | 7,649,640 | 7,535,259 | ||||||||

| Interest-bearing | 41,394,817 | 40,119,937 | ||||||||

| 4 | 49,044,457 | 47,655,196 | ||||||||

| Cash collateral, reverse repurchase agreements and securities borrowing | 5(a) | 2,177,200 | 1,033,177 | |||||||

| Investments: | ||||||||||

| At fair value through profit or loss | 6(a) | 4,957,236 | 4,715,343 | |||||||

| At fair value through other comprehensive income | 33,043,160 | 34,208,187 | ||||||||

| At fair value through other comprehensive income | ||||||||||

| pledged as collateral | 5,990,889 | 5,934,451 | ||||||||

| 6(b) | 39,034,049 | 40,142,638 | ||||||||

| Amortized cost | 8,490,126 | 7,904,517 | ||||||||

| Amortized cost pledged as collateral | 323,531 | 1,063,360 | ||||||||

| 6(c) | 8,813,657 | 8,967,877 | ||||||||

| Loans, net: | 7 | |||||||||

| Loans, net of unearned income | 149,984,954 | 145,732,273 | ||||||||

| Allowance for loan losses | (7,669,950 | ) | (7,994,977 | ) | ||||||

| 142,315,004 | 137,737,296 | |||||||||

| Financial assets designated at fair value through | ||||||||||

| profit or loss | 3(f) | 992,429 | 932,734 | |||||||

| Reinsurance contract assets | 8(a) | 708,560 | 841,170 | |||||||

| Property, furniture and equipment, net | 9 | 2,069,017 | 1,438,609 | |||||||

| Due from customers on banker’s acceptances | 7(b) | 345,906 | 528,184 | |||||||

| Intangible assets, goodwill and others, net | 10 | 4,764,394 | 3,289,157 | |||||||

| Right-of-use assets, net | 11(a) | 603,441 | 402,538 | |||||||

| Deferred tax assets, net | 17(c) | 1,391,636 | 1,170,866 | |||||||

| Other assets | 12 | 10,145,547 | 7,234,155 | |||||||

| Total assets | 267,362,533 | 256,088,940 | ||||||||

| Note | 2025 | 2024 | ||||||||

| S/(000) | S/(000) | |||||||||

| Liabilities | ||||||||||

| Deposits and obligations: | ||||||||||

| Non-interest-bearing | 52,217,286 | 47,160,191 | ||||||||

| Interest-bearing | 118,184,347 | 114,681,875 | ||||||||

| 13(a) | 170,401,633 | 161,842,066 | ||||||||

| Payables from repurchase agreements and securities lending | 5(b) | 8,243,787 | 9,060,710 | |||||||

| Due to banks and correspondents | 14(a) | 10,675,238 | 10,754,385 | |||||||

| Due from customers on banker’s acceptances | 3(n) | 345,906 | 528,184 | |||||||

| Lease liabilities | 11(b) | 612,259 | 404,817 | |||||||

| Financial liabilities at fair value through profit or loss | 3(y) | 1,055,893 | 151,485 | |||||||

| Insurance contract liabilities | 8(b) | 14,264,155 | 13,422,285 | |||||||

| Bonds and notes issued | 15 | 14,025,535 | 17,268,443 | |||||||

| Deferred tax liabilities, net | 17(c) | 376,939 | 59,025 | |||||||

| Other liabilities | 12 | 8,265,079 | 7,620,306 | |||||||

| Total liabilities | 228,266,424 | 221,111,706 | ||||||||

| Equity | 16 | |||||||||

| Equity attributable to Credicorp's equity holders: | ||||||||||

| Capital stock | 1,318,993 | 1,318,993 | ||||||||

| Treasury stock | (209,845 | ) | (208,879 | ) | ||||||

| Capital surplus | 148,729 | 176,307 | ||||||||

| Reserves | 29,648,582 | 27,202,665 | ||||||||

| Other reserves | 544,767 | 214,627 | ||||||||

| Retained earnings | 6,915,724 | 5,642,738 | ||||||||

| 38,366,950 | 34,346,451 | |||||||||

| Non-controlling interests | 729,159 | 630,783 | ||||||||

| Total equity | 39,096,109 | 34,977,234 | ||||||||

| Total liabilities and equity | 267,362,533 | 256,088,940 | ||||||||

|

|

The accompanying notes are an integral part of these consolidated financial statements.

CREDICORP LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF INCOME

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023

| Note | 2025 | 2024 | 2023 | ||||||||||||

| S/(000) | S/(000) | S/(000) | |||||||||||||

| Interest and similar income | 19 | 19,930,169 | 19,869,256 | 18,798,495 | |||||||||||

| Interest and similar expenses | 19 | (5,213,690 | ) | (5,754,125 | ) | (5,860,523 | ) | ||||||||

| Net interest, similar income and expenses | 14,716,479 | 14,115,131 | 12,937,972 | ||||||||||||

| Provision for credit losses on loan portfolio | 7(c) | (2,873,454 | ) | (3,943,301 | ) | (3,957,143 | ) | ||||||||

| Recoveries of written-off loans | 467,198 | 423,854 | 334,798 | ||||||||||||

| Provision for credit losses on loan portfolio, net of recoveries | (2,406,256 | ) | (3,519,447 | ) | (3,622,345 | ) | |||||||||

| Net interest, similar income and expenses, after provision for credit losses on loan portfolio | 12,310,223 | 10,595,684 | 9,315,627 | ||||||||||||

| Other income | |||||||||||||||

| Commissions and fees | 20 | 4,199,719 | 4,052,103 | 3,804,459 | |||||||||||

| Net gain on foreign exchange transactions | 1,542,318 | 1,359,805 | 886,126 | ||||||||||||

| Net gain on securities | 21 | 400,686 | 362,295 | 425,144 | |||||||||||

| Net gain on derivatives held for trading | 51,917 | 156,195 | 53,665 | ||||||||||||

| Net exchange difference result | 41,991 | (41,058 | ) | 45,778 | |||||||||||

| Others | 25 | 584,648 | 514,779 | 440,653 | |||||||||||

| Total other income | 6,821,279 | 6,404,119 | 5,655,825 | ||||||||||||

| Insurance and reinsurance result | |||||||||||||||

| Insurance service result | 22 | 1,848,025 | 1,693,617 | 1,602,421 | |||||||||||

| Reinsurance result | 22 | (458,825 | ) | (494,597 | ) | (391,321 | ) | ||||||||

| Total insurance and reinsurance result | 1,389,200 | 1,199,020 | 1,211,100 | ||||||||||||

| Medical services results | |||||||||||||||

| Sales of medical services and medicines | 3(d) | 1,387,341 | – | – | |||||||||||

| Cost of sales of medical services and medicines | 3(d) | (972,707 | ) | – | – | ||||||||||

| Total medical services results | 414,634 | – | – | ||||||||||||

| Other expenses | |||||||||||||||

| Salaries and employee benefits | 23 | (5,435,471 | ) | (4,676,436 | ) | (4,265,453 | ) | ||||||||

| Administrative expenses | 24 | (4,090,784 | ) | (4,183,775 | ) | (3,803,203 | ) | ||||||||

| Depreciation and amortization | 9(a) and 10(a) | (746,243 | ) | (570,830 | ) | (511,174 | ) | ||||||||

| Impairment loss on goodwill | 10(b) | – | (27,346 | ) | (71,959 | ) | |||||||||

| Depreciation of right-of-use assets | 11(a) | (146,899 | ) | (142,640 | ) | (147,833 | ) | ||||||||

| Others | 25 | (568,386 | ) | (773,269 | ) | (534,601 | ) | ||||||||

| Total other expenses | (10,987,783 | ) | (10,374,296 | ) | (9,334,223 | ) | |||||||||

CONSOLIDATED STATEMENT OF INCOME

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023 (CONTINUED)

| Note | 2025 | 2024 | 2023 | ||||||||||||

| S/(000) | S/(000) | S/(000) | |||||||||||||

| Net result before income tax | 9,947,553 | 7,824,527 | 6,848,329 | ||||||||||||

| Income tax | 17(b) | (2,864,899 | ) | (2,201,275 | ) | (1,888,451 | ) | ||||||||

| Net result after income tax | 7,082,654 | 5,623,252 | 4,959,878 | ||||||||||||

| Attributable to: | |||||||||||||||

| Credicorp’s equity holders | 6,925,377 | 5,501,254 | 4,865,540 | ||||||||||||

| Non-controlling interests | 157,277 | 121,998 | 94,338 | ||||||||||||

| 7,082,654 | 5,623,252 | 4,959,878 | |||||||||||||

| Net basic and dilutive earnings per share attributable to Credicorp's equity holders (in Soles): | |||||||||||||||

| Basic | 26 | 87.25 | 69.24 | 61.22 | |||||||||||

| Diluted | 26 | 87.08 | 69.09 | 61.08 | |||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

CREDICORP LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023

| 2025 | 2024 | 2023 | |||||||||||||

| S/(000) | S/(000) | S/(000) | |||||||||||||

| Net result after income tax | 7,082,654 | 5,623,252 | 4,959,878 | ||||||||||||

| Other comprehensive income: | |||||||||||||||

| To be reclassified to profit or loss in subsequent periods, net of income tax: | |||||||||||||||

| Net gain on investments at fair value through other comprehensive income | 16(d) | 1,259,728 | 205,765 | 1,334,943 | |||||||||||

| Income tax | 16(d) | 24,152 | 5,118 | (58,489 | ) | ||||||||||

| 1,283,880 | 210,883 | 1,276,454 | |||||||||||||

| Net movement of cash flow hedge reserves | 16(d) | 3,464 | 13,925 | (17,443 | ) | ||||||||||

| Income tax | 16(d) | (1,575 | ) | (4,030 | ) | 5,104 | |||||||||

| 1,889 | 9,895 | (12,339 | ) | ||||||||||||

| Insurance reserves | 16(d) | (523,992 | ) | (70,176 | ) | (762,811 | ) | ||||||||

| (523,992 | ) | (70,176 | ) | (762,811 | ) | ||||||||||

| Exchange differences on translation of foreign operations | 16(d) | (406,955 | ) | (114,142 | ) | 73,464 | |||||||||

| Net movement in hedges of net investments in foreign businesses | 16(d) | – | – | 18,950 | |||||||||||

| (406,955 | ) | (114,142 | ) | 92,414 | |||||||||||

| Total | 354,822 | 36,460 | 593,718 | ||||||||||||

| Not to be reclassified to profit or loss in subsequent periods: | |||||||||||||||

| Net (loss) gain on equity instruments designated at fair value through other comprehensive income | 16(d) | (18,599 | ) | 15,684 | (8,329 | ) | |||||||||

| Transfer of the fair value reserve of equity instruments to retained earnings | 16(d) | 8,336 | (137,787 | ) | – | ||||||||||

| Income tax | 16(d) | (2,332 | ) | 8,439 | (3,791 | ) | |||||||||

| Total | (12,595 | ) | (113,664 | ) | (12,120 | ) | |||||||||

| Total other comprehensive income | 16(d) | 342,227 | (77,204 | ) | 581,598 | ||||||||||

| Total comprehensive income for the period, net of income tax | 7,424,881 | 5,546,048 | 5,541,476 | ||||||||||||

| Attributable to: | |||||||||||||||

| Credicorp's equity holders | 7,255,517 | 5,420,098 | 5,437,495 | ||||||||||||

| Non-controlling interest | 169,364 | 125,950 | 103,981 | ||||||||||||

| 7,424,881 | 5,546,048 | 5,541,476 | |||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

CREDICORP LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023

| Attributable to Credicorp's equity holders. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other reserves | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Treasury stock | Instruments that will not be reclassified to income | Instruments that will be reclassified to the consolidated statement of income | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital stock | Shares of the Group | Share-based payment | Capital surplus | Reserves |

Investments in equity instruments |

Investments in debt instruments |

Cash flow hedge reserve | Insurance reserves | Foreign currency translation reserve | Retained earnings | Total | Non-controlling interest |

Total equity |

|||||||||||||||||||||||||||||||||||||||||||

| S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||||||||||||||||||||||||||

| Balances as of January 1, 2023 | 1,318,993 | (204,326 | ) | (3,192 | ) | 231,556 | 23,659,626 | 170,408 | (1,655,559 | ) | 788 | 1,133,536 | 74,655 | 4,277,159 | 29,003,644 | 591,569 | 29,595,213 | |||||||||||||||||||||||||||||||||||||||

| Changes in equity in 2023 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net result after income tax | – | – | – | – | – | – | – | – | – | – | 4,865,540 | 4,865,540 | 94,338 | 4,959,878 | ||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income, Note 16(d) | – | – | – | – | – | (12,247 | ) | 1,258,137 | (12,191 | ) | (754,192 | ) | 92,448 | – | 571,955 | 9,643 | 581,598 | |||||||||||||||||||||||||||||||||||||||

| Total comprehensive income | – | – | – | – | – | (12,247 | ) | 1,258,137 | (12,191 | ) | (754,192 | ) | 92,448 | 4,865,540 | 5,437,495 | 103,981 | 5,541,476 | |||||||||||||||||||||||||||||||||||||||

| Transfer of retained earnings to reserves, Note 16(c) | – | – | – | – | 2,593,598 | – | – | – | – | – | (2,593,598 | ) | – | – | – | |||||||||||||||||||||||||||||||||||||||||

| Dividend distribution, Note 16(e) | – | – | – | – | – | – | – | – | – | – | (1,994,037 | ) | (1,994,037 | ) | – | (1,994,037 | ) | |||||||||||||||||||||||||||||||||||||||

| Dividends paid to non-controlling interest of subsidiaries | – | – | – | – | – | – | – | – | – | – | – | – | (62,051 | ) | (62,051 | ) | ||||||||||||||||||||||||||||||||||||||||

| Subsidiary acquisition | – | – | – | – | – | – | – | – | – | – | – | – | 14,192 | 14,192 | ||||||||||||||||||||||||||||||||||||||||||

| Minority purchase | – | – | – | – | – | – | – | – | – | – | – | – | (1,773 | ) | (1,773 | ) | ||||||||||||||||||||||||||||||||||||||||

| Purchase of treasury stock, Note 16(b) | – | – | (2,279 | ) | (83,296 | ) | – | – | – | – | – | – | – | (85,575 | ) | – | (85,575 | ) | ||||||||||||||||||||||||||||||||||||||

| Share-based payment transactions | – | – | 1,764 | 79,979 | (12,225 | ) | – | – | – | – | – | – | 69,518 | – | 69,518 | |||||||||||||||||||||||||||||||||||||||||

| Dividends not collected | – | – | – | – | 11,579 | – | – | – | – | – | – | 11,579 | – | 11,579 | ||||||||||||||||||||||||||||||||||||||||||

| Result from exchange of strategic shares | – | – | – | – | – | – | – | – | – | – | 14,425 | 14,425 | – | 14,425 | ||||||||||||||||||||||||||||||||||||||||||

| Others | – | – | – | – | – | – | – | – | – | – | 2,955 | 2,955 | 1,143 | 4,098 | ||||||||||||||||||||||||||||||||||||||||||

| Balances as of December 31, 2023 | 1,318,993 | (204,326 | ) | (3,707 | ) | 228,239 | 26,252,578 | 158,161 | (397,422 | ) | (11,403 | ) | 379,344 | 167,103 | 4,572,444 | 32,460,004 | 647,061 | 33,107,065 | ||||||||||||||||||||||||||||||||||||||

| Balances as of January 1, 2024 | 1,318,993 | (204,326 | ) | (3,707 | ) | 228,239 | 26,252,578 | 158,161 | (397,422 | ) | (11,403 | ) | 379,344 | 167,103 | 4,572,444 | 32,460,004 | 647,061 | 33,107,065 | ||||||||||||||||||||||||||||||||||||||

| Changes in equity in 2024 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net result after income tax | – | – | – | – | – | – | – | – | – | – | 5,501,254 | 5,501,254 | 121,998 | 5,623,252 | ||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income, Note 16(d) | – | – | – | – | – | 24,116 | 206,271 | 9,770 | (69,383 | ) | (114,143 | ) | – | 56,631 | 3,952 | 60,583 | ||||||||||||||||||||||||||||||||||||||||

| Transfer of fair value reserve to accumulated results, Note 16(d) | – | – | – | – | – | (137,787 | ) | – | – | – | – | – | (137,787 | ) | – | (137,787 | ) | |||||||||||||||||||||||||||||||||||||||

| Total comprehensive income | – | – | – | – | – | (113,671 | ) | 206,271 | 9,770 | (69,383 | ) | (114,143 | ) | 5,501,254 | 5,420,098 | 125,950 | 5,546,048 | |||||||||||||||||||||||||||||||||||||||

| Transfer of fair value reserve of equity instruments designated at FVOCI due to Sale of Alicorp shares | – | – | – | – | – | – | – | – | – | – | 137,787 | 137,787 | – | 137,787 | ||||||||||||||||||||||||||||||||||||||||||

| Transfer of retained earnings to reserves, Note 16(c) | – | – | – | – | 1,778,787 | – | – | – | – | – | (1,778,787 | ) | – | – | – | |||||||||||||||||||||||||||||||||||||||||

| Dividend distribution, Note 16(e) | – | – | – | – | – | – | – | – | – | – | (2,788,657 | ) | (2,788,657 | ) | – | (2,788,657 | ) | |||||||||||||||||||||||||||||||||||||||

| Distribution of extraordinary dividends, Note 16(e) | – | – | – | – | (875,991 | ) | – | – | – | – | – | – | (875,991 | ) | – | (875,991 | ) | |||||||||||||||||||||||||||||||||||||||

| Dividends paid to non-controlling interest of subsidiaries | – | – | – | – | – | – | – | – | – | – | – | – | (106,922 | ) | (106,922 | ) | ||||||||||||||||||||||||||||||||||||||||

| Minority purchase Mibanco Colombia | – | – | – | – | 42,964 | – | – | – | – | – | – | 42,964 | (36,781 | ) | 6,183 | |||||||||||||||||||||||||||||||||||||||||

| Purchase of treasury stock, Note 16(b) | – | – | (2,434 | ) | (108,460 | ) | – | – | – | – | – | – | – | (110,894 | ) | – | (110,894 | ) | ||||||||||||||||||||||||||||||||||||||

| Share-based payment transactions | – | – | 1,588 | 56,528 | (954 | ) | – | – | – | – | – | – | 57,162 | – | 57,162 | |||||||||||||||||||||||||||||||||||||||||

| Dividends not collected | – | – | – | – | 5,281 | – | – | – | – | – | – | 5,281 | – | 5,281 | ||||||||||||||||||||||||||||||||||||||||||

| Others | – | – | – | – | – | – | – | – | – | – | (1,303 | ) | (1,303 | ) | 1,475 | 172 | ||||||||||||||||||||||||||||||||||||||||

| Balances as of December 31, 2024 | 1,318,993 | (204,326 | ) | (4,553 | ) | 176,307 | 27,202,665 | 44,490 | (191,151 | ) | (1,633 | ) | 309,961 | 52,960 | 5,642,738 | 34,346,451 | 630,783 | 34,977,234 | ||||||||||||||||||||||||||||||||||||||

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023 (CONTINUED)

| Attributable to Credicorp's equity holders. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other reserves | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Treasury stock | Instruments that will not be reclassified to income | Instruments that will be reclassified to the consolidated statement of income | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Capital stock | Shares of the Group | Share-based payment | Capital surplus | Reserves |

Investments in equity instruments |

Investments in debt instruments |

Cash flow hedge reserve | Insurance reserves | Foreign currency translation reserve | Retained earnings | Total | Non-controlling interest |

Total equity |

|||||||||||||||||||||||||||||||||||||||||||

| S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||||||||||||||||||||||||||

| Balances as of January 1, 2025 | 1,318,993 | (204,326 | ) | (4,553 | ) | 176,307 | 27,202,665 | 44,490 | (191,151 | ) | (1,633 | ) | 309,961 | 52,960 | 5,642,738 | 34,346,451 | 630,783 | 34,977,234 | ||||||||||||||||||||||||||||||||||||||

| Changes in equity in 2025 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net result after income tax | – | – | – | – | – | – | – | – | – | – | 6,925,377 | 6,925,377 | 157,277 | 7,082,654 | ||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income, Note 16(d) | – | – | – | – | – | (20,927 | ) | 1,265,461 | 1,860 | (518,071 | ) | (406,519 | ) | – | 321,804 | 12,087 | 333,891 | |||||||||||||||||||||||||||||||||||||||

| Transfer of the fair value reserve of equity instruments designated at FVOCI for sale, Note 16(d) | – | – | – | – | – | 8,336 | – | – | – | – | – | 8,336 | – | 8,336 | ||||||||||||||||||||||||||||||||||||||||||

| Total comprehensive income | – | – | – | – | – | (12,591 | ) | 1,265,461 | 1,860 | (518,071 | ) | (406,519 | ) | 6,925,377 | 7,255,517 | 169,364 | 7,424,881 | |||||||||||||||||||||||||||||||||||||||

| Transfer of retained earnings to reserves, Note 16(c) | – | – | – | – | 5,637,738 | – | – | – | – | – | (5,637,738 | ) | – | – | – | |||||||||||||||||||||||||||||||||||||||||

| Dividend distribution, Note 16(e) | – | – | – | – | (3,181,454 | ) | – | – | – | – | – | – | (3,181,454 | ) | – | (3,181,454 | ) | |||||||||||||||||||||||||||||||||||||||

| Dividends paid to non-controlling interest of subsidiaries | – | – | – | – | – | – | – | – | – | – | – | – | (120,855 | ) | (120,855 | ) | ||||||||||||||||||||||||||||||||||||||||

| Purchase of treasury stock, Note 16(b) | – | – | (2,451 | ) | (116,800 | ) | – | – | – | – | – | – | – | (119,251 | ) | – | (119,251 | ) | ||||||||||||||||||||||||||||||||||||||

| Share-based payment transactions | – | – | 1,485 | 89,222 | 64,746 | – | – | – | – | – | – | 155,453 | – | 155,453 | ||||||||||||||||||||||||||||||||||||||||||

| Release of optional reserve | – | – | – | – | (76,441 | ) | – | – | – | – | – | – | (76,441 | ) | – | (76,441 | ) | |||||||||||||||||||||||||||||||||||||||

| Non-controlling interest from Pacifico EPS, Note 2(a) | – | – | – | – | – | – | – | – | – | – | – | – | 57,177 | 57,177 | ||||||||||||||||||||||||||||||||||||||||||

| Minority purchase | – | – | – | – | – | – | – | – | – | – | (9,142 | ) | (9,142 | ) | (8,783 | ) | (17,925 | ) | ||||||||||||||||||||||||||||||||||||||

| Transfer of fair value reserve of equity instruments designated at FVOCI for sale | – | – | – | – | – | – | – | – | – | – | (8,336 | ) | (8,336 | ) | – | (8,336 | ) | |||||||||||||||||||||||||||||||||||||||

| Dividends not collected | – | – | – | – | 1,314 | – | – | – | – | – | – | 1,314 | – | 1,314 | ||||||||||||||||||||||||||||||||||||||||||

| Others | – | – | – | – | 14 | – | – | – | – | – | 2,825 | 2,839 | 1,473 | 4,312 | ||||||||||||||||||||||||||||||||||||||||||

| Balances as of December 31, 2025 | 1,318,993 | (204,326 | ) | (5,519 | ) | 148,729 | 29,648,582 | 31,899 | 1,074,310 | 227 | (208,110 | ) | (353,559 | ) | 6,915,724 | 38,366,950 | 729,159 | 39,096,109 | ||||||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

CREDICORP LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023

| Note | 2025 | 2024 | 2023 | |||||||||

| S/(000) | S/(000) | S/(000) | ||||||||||

| CASH AND CASH EQUIVALENTS FROM OPERATING ACTIVITIES | ||||||||||||

| Net result after income tax | 7,082,654 | 5,623,252 | 4,959,878 | |||||||||

| Adjustment to reconcile net profit to net cash arising from operating activities: | ||||||||||||

| Provision for credit losses on loan portfolio | 7(c) | 2,873,454 | 3,943,301 | 3,957,143 | ||||||||

| Depreciation and amortization | 9(a) and 10(a) | 746,243 | 570,830 | 511,174 | ||||||||

| Depreciation of right-of-use assets | 11(a) | 146,899 | 142,640 | 147,833 | ||||||||

| Depreciation of investment properties | 12(g) | 8,803 | 9,098 | 8,115 | ||||||||

| Provision for sundry risks | 25 | 149,651 | 315,214 | 95,873 | ||||||||

| Deferred income tax | 17(b) | (125,724 | ) | (54,943 | ) | (76,088 | ) | |||||

| Net gain on sale of securities | 21 | (400,686 | ) | (362,295 | ) | (425,144 | ) | |||||

| Impairment loss on goodwill | 10(b) | – | 27,346 | 71,959 | ||||||||

| Net gain of trading derivatives | (51,917 | ) | (156,195 | ) | (53,665 | ) | ||||||

| Net gain from sale of property, furniture and equipment | 25 | (37,636 | ) | (68,037 | ) | (1,654 | ) | |||||

| Net gain from sale of foreclosed assets | (30,139 | ) | (27,172 | ) | 1,867 | |||||||

| Expense for share-based payment transactions | 23 | 149,037 | 104,848 | 83,328 | ||||||||

| Net gain from sale of loan portfolio | 25 | (1,778 | ) | (21,295 | ) | (83,515 | ) | |||||

| Intangible losses due to withdrawals and dismissed projects | 25 | 79,335 | 131,142 | 96,978 | ||||||||

| Gain on remeasurement of previously held equity interest in Pacifico Entidad Prestadora de Salud | 25 | (235,490 | ) | – | – | |||||||

| Others | 65,027 | 145,492 | 3,005 | |||||||||

| Net changes in assets and liabilities | ||||||||||||

| Net (increase) decrease in assets: | ||||||||||||

| Loans | (13,447,331 | ) | (4,461,273 | ) | (1,105,306 | ) | ||||||

| Investments at fair value through profit or loss | (204,871 | ) | 412,376 | (456,626 | ) | |||||||

| Investments at fair value through other comprehensive income | 1,459,872 | (2,555,702 | ) | (5,164,701 | ) | |||||||

| Cash collateral, reverse repurchase agreements and securities borrowings | (1,251,363 | ) | 383,427 | (330,448 | ) | |||||||

| Sale of written off portfolio | 7,320 | 55,230 | 239,599 | |||||||||

| Claim filed with the Tax Authority | 12(a) and 31 | (1,577,175 | ) | – | – | |||||||

| Other assets | (2,045,992 | ) | (1,111,692 | ) | 520,331 |

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023 (CONTINUED)

| Note | 2025 | 2024 | 2023 | |||||||||

| S/(000) | S/(000) | S/(000) | ||||||||||

|

Net increase (decrease) in liabilities

|

||||||||||||

| Deposits and obligations | 17,248,164 | 13,286,449 | 2,271,524 | |||||||||

| Due to Banks and correspondents | 379,613 | (1,600,761 | ) | 3,455,502 | ||||||||

| Payables from repurchase agreements and securities lending | (704,293 | ) | (1,111,676 | ) | (2,790,671 | ) | ||||||

| Bonds and notes issued | (4,054,938 | ) | 348,532 | (2,213,122 | ) | |||||||

| Short-term and low-value lease payments | (143,855 | ) | (118,156 | ) | (108,357 | ) | ||||||

| Other liabilities | 5,183,948 | 2,375,248 | 2,604,047 | |||||||||

| Net income for the period after the net change in assets and liabilities, and adjustments | 11,266,832 | 16,225,228 | 6,218,859 | |||||||||

| Income tax paid | (2,660,631 | ) | (1,703,135 | ) | (2,139,140 | ) | ||||||

| Net cash flow from operating activities | 8,606,201 | 14,522,093 | 4,079,719 | |||||||||

| NET CASH FLOWS FROM INVESTING ACTIVITIES | ||||||||||||

| Proceeds from sale of property, furniture and equipment | 160,264 | 98,223 | 53,152 | |||||||||

| Proceeds from sale of investment property | 1,282 | 47,100 | – | |||||||||

| Collections for maturities and coupons of investment at amortized cost | 859,930 | 1,740,670 | 1,245,434 | |||||||||

| Purchase of property, furniture and equipment | 9 | (284,710 | ) | (310,144 | ) | (322,371 | ) | |||||

| Purchase of investment property | 12(g) | (183,563 | ) | (70,399 | ) | (37,667 | ) | |||||

| Purchase of intangible assets | 10(a) | (983,971 | ) | (801,290 | ) | (828,803 | ) | |||||

| Purchase of investment at amortized cost | (255,185 | ) | (176,601 | ) | (1,359,245 | ) | ||||||

| Acquisition of Pacifico EPS shares, net cash acquired | 2(a) | (727,180 | ) | – | (5,564 | ) | ||||||

| Termination of the Joint Venture Agreement | (180,000 | ) | – | – | ||||||||

| Net cash flows from investing activities | (1,593,133 | ) | 527,559 | (1,255,064 | ) | |||||||

| NET CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||||||

| Dividends paid | 16(e) | (3,181,454 | ) | (3,664,648 | ) | (1,994,037 | ) | |||||

| Dividends paid to non-controlling interest of subsidiaries | (120,855 | ) | (106,777 | ) | (62,051 | ) | ||||||

| Principal payments of leasing contracts | (152,899 | ) | (152,693 | ) | (157,386 | ) | ||||||

| Interest payments of leasing contracts | (37,169 | ) | (22,828 | ) | (25,574 | ) | ||||||

| Purchase of treasury stock | 16(b) | (119,251 | ) | (110,894 | ) | (85,575 | ) | |||||

| Purchase of non-controlling interest of subsidiaries | (17,925 | ) | (36,781 | ) | (1,773 | ) | ||||||

| Subordinated bonds, net | 1,791,983 | 2,284,200 | 62,044 | |||||||||

| Net cash flows from financing activities | (1,837,570 | ) | (1,810,421 | ) | (2,264,352 | ) | ||||||

| Net increase of cash and cash equivalents before effect of changes in exchange rate | 5,175,498 | 13,239,231 | 560,303 | |||||||||

| Effect of changes in exchange rate of cash and cash equivalents | (3,771,899 | ) | 410,258 | (760,651 | ) | |||||||

| Cash and cash equivalents at the beginning of the period | 47,570,103 | 33,920,614 | 34,120,962 | |||||||||

| Cash and cash equivalents at the end of the period | 4(a) | 48,973,702 | 47,570,103 | 33,920,614 |

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023 (CONTINUED)

| Note | 2025 | 2024 | 2023 | ||||||||||

| S/(000) | S/(000) | S/(000) | |||||||||||

| Additional information from cash flows | |||||||||||||

| Interest received | 19,973,931 | 19,896,077 | 18,658,791 | ||||||||||

| Interest paid | (5,160,077 | ) | (5,852,580 | ) | (5,080,522 | ) | |||||||

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2025, 2024 AND 2023 (CONTINUED)

Reconciliation of liabilities arising from financing activities:

| Changes that generate cash flows | Changes that do not generate cash flows | |||||||||||||||||||||||

| 2025 | As of January 1, 2025 | Received | Paid |

Exchange difference |

Others | As of December 31, 2025 | ||||||||||||||||||

| S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||

| Subordinated bonds | 8,016,712 | 4,842,529 | (3,050,546 | ) | (967,963 | ) | (3,013 | ) | 8,837,719 | |||||||||||||||

| Lease liabilities | 404,817 | – | (190,068 | ) | (31,727 | ) | 429,237 | 612,259 | ||||||||||||||||

| 8,421,529 | 4,842,529 | (3,240,614 | ) | (999,690 | ) | 426,224 | 9,449,978 | |||||||||||||||||

| Changes that generate cash flows | Changes that do not generate cash flows | |||||||||||||||||||||||

| 2024 | As of January 1, 2024 | Received | Paid |

Exchange difference |

Others | As of December 31, 2024 | ||||||||||||||||||

| S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||

| Subordinated bonds | 5,680,120 | 2,284,200 | – | 48,509 | 3,883 | 8,016,712 | ||||||||||||||||||

| Lease liabilities | 512,579 | – | (175,521 | ) | 3,986 | 63,773 | 404,817 | |||||||||||||||||

| 6,192,699 | 2,284,200 | (175,521 | ) | 52,495 | 67,656 | 8,421,529 | ||||||||||||||||||

| Changes that generate cash flows | Changes that do not generate cash flows | |||||||||||||||||||||||

| 2023 | As of January 1, 2023 | Received | Paid |

Exchange difference |

Others | As of December 31, 2023 | ||||||||||||||||||

| S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||

| Subordinated bonds | 5,738,414 | 284,944 | (222,900 | ) | (150,568 | ) | 30,230 | 5,680,120 | ||||||||||||||||

| Lease liabilities | 578,074 | – | (182,960 | ) | (8,627 | ) | 126,092 | 512,579 | ||||||||||||||||

| 6,316,488 | 284,944 | (405,860 | ) | (159,195 | ) | 156,322 | 6,192,699 | |||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

CREDICORP LTD. AND SUBSIDIARIES

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

AS OF DECEMBER 31, 2025 AND 2024

|

1 |

OPERATIONS |

Credicorp Ltd. (hereinafter “Credicorp” or the “Group”) is a limited liability company incorporated in Bermuda in 1995 to act as a holding company and according to Bermuda's economic substance regulation, Credicorp Ltd. as an independent legal entity, is considered a “Pure Equity Holding Entity” (PEHE). Credicorp's activity is to maintain equity interests and receive passive income such as dividends, capital gains and other income from investments in securities.

In order to keep Credicorp's structure and organization fully aligned with the new legislation on economic substance approved by the Government of Bermuda on January 11, 2019, the decisions of the Credicorp Board of Directors will be limited to issues related to Credicorp's strategy, objectives and goals, main action plans and policies, annual budgets, business plans and control of their implementation, supervision of the main expenses, investments, acquisitions and disposals, among other “passive” decisions related to Credicorp. The authority to make decisions applicable to Credicorp's subsidiaries, such as the adoption of relevant strategic or management decisions, the assumption of expenses for the benefit of its affiliates, the coordination of group activities, and the granting of credit facilities in favor of its affiliates, it has been transferred to Grupo Crédito S.A., a subsidiary of Credicorp.

Credicorp, through its banking and non-banking subsidiaries and its subsidiary Pacífico S.A. Entidad Prestadora de Salud (hereinafter Pacífico EPS), offers a wide range of financial, insurance and health services and products, mainly throughout Peru and in other countries (see Note 3 (b). Its main subsidiary is Banco de Crédito del Perú (hereinafter “BCP” or the “Bank”), a multiple bank incorporated in Perú.

Credicorp's legal address is Clarendon House 2 Church Street Hamilton, Bermuda; likewise, the main offices from where Credicorp's businesses are managed are located at Calle Centenario N° 156, La Molina, Lima, Perú.

The consolidated financial statements as of December 31, 2024, and for the year ended on that date were approved and authorized for issuance by the Board of Directors and Management on February 27, 2025, and presented for the Annual General Shareholders Meeting on March 27, 2025. The consolidated financial statements as of December 31, 2025, and for the year ended on that date, were approved by the Management on February 26,2025, and will be presented for final approval in the Annual General Meeting of Shareholders, which will be held within the deadlines established by law.

Credicorp is listed on the Lima and New York Stock Exchanges.

|

2 |

BUSINESS ACQUISITIONS |

| a) | Acquisition of a majority interest in Pacífico EPS |

On November 01, 2024 Credicorp entered into an agreement to acquire the 50.0 percent interest from Empresas Banmédica (“Banmédica” hereafter) in the partnership and participation agreement entered into in December 2014 between Pacifico Compañía de Seguros y Reaseguros S.A. (“Pacifico Seguros”) and Banmédica.

Pursuant to this acquisition, Banmédica trasnfered its 50.0 percent interest in the private health insurance business in Peru (Joint Venture Agreement) to Pacifico Seguros. In addition, Banmédica transfered its 50.0 percent interest in Pacifico S.A. Entidad Prestadora de Salud (“Pacifico EPS”), which manages the corporate employee health insurance and medical services businesses in Peru, to Credicorp's subsidiary, Grupo Crédito S.A.

As of March 13, 2025, the Company completed the acquisition of the remaining 50.0 percent interest in Pacífico EPS (representing 24,627,219 shares) and 50.0 percent of the co-investment agreement with Banmédica. The consideration paid for the acquisition of the interest in Pacífico EPS amounted to S/950.9 million.

The business combination was recognized using the acquisition method in accordance with IFRS 3 "Business Combinations". A business combination achieved in stages requires the acquirer to remeasure its previously held equity interest at fair value at the acquisition date, with any resulting gain or loss recognized in profit or loss. Accordingly, the Group remeasured its previously held interest in Pacifico EPS at fair value, recognizing a gain of S/235.5 million, see Note 25.

At the date of acquisition, the carrying amount and fair value of the identified assets and liabilities of the entities purchased were the following:

| Carrying amount | Fair value adjustments | Fair value recognized at acquisition | |||||||

| S/(000) | S/(000) | S/(000) | |||||||

| Assets | |||||||||

| Cash | 223,670 | – | 223,670 | ||||||

| Investments | 320,161 | – | 320,161 | ||||||

| Property, furniture and equipment, net, Note 9(a) | 522,895 | 208,821 | 731,716 | ||||||

| Investment property, Note 12(g) | 948 | 5 | 953 | ||||||

| Right-of-use assets, net, Note 11 | 128,049 | – | 128,049 | ||||||

| Intangible assets, Note 10(a) | 27,036 | 681,571 | 708,607 | ||||||

| Other assets | 484,974 | – | 484,974 | ||||||

| Total assets | 1,707,733 | 890,397 | 2,598,130 | ||||||

| Liabilities | |||||||||

| Due to banks and correspondents | 15,795 | – | 15,795 | ||||||

| Bonds and notes issued | 115,520 | – | 115,520 | ||||||

| Lease liabilities | 156,245 | – | 156,245 | ||||||

| Deferred tax liabilities, net | 2,375 | 262,667 | 265,042 | ||||||

| Other liabilities | 615,150 | – | 615,150 | ||||||

| Total liabilities | 905,085 | 262,667 | 1,167,752 | ||||||

| Total net assets identified at fair value | 802,648 | 627,730 | 1,430,378 | ||||||

| Existing shareholding | (950,850 | ) | |||||||

| Non-controlling interest | (57,177 | ) | |||||||

| Goodwill arising on acquisition, Note 10(b) | 528,499 | ||||||||

| Total purchase consideration | 950,850 | ||||||||

| Analysis of cash flows on acquisition | |||||||||

| Net cash acquired with the subsidiary (included in investing cash flows) | 223,670 | ||||||||

| Cash paid | (950,850 | ) | |||||||

| Net cash flow on acquisition | (727,180 | ) |

The fair value at the acquisition date and the carrying amount of trade receivables amount to S/271.2 million, which are included under “other assets”, and the full contractual amounts were collected.

From the date of acquisition, Pacifico EPS has contributed S/524.4 million of net operating income and S/153.4 million to net profit before tax from the continuing operations of the Group. If the acquisition had taken place at the beginning of the year, net operating income from continuing operations would have been S/611.4 million and the profit before tax from continuing operations for the period would have been S/190.3 million.

The goodwill recognized reflects the market position of the acquired business and the anticipated benefits associated with its continuing operations. It is not expected to be deductible for income tax purposes.

| b) | Agreement to Acquire Shares of Helm Bank USA – |

On December 29, 2025, Banco de Crédito del Perú (“BCP”) entered into a Stock Purchase Agreement (“SPA”) with the shareholders of Helm Bank USA to acquire 100.0 percent of the issued and outstanding shares of Helm Bank USA (“Helm Bank”). Pursuant to the terms of the SPA, BCP will pay an amount of US$180.0 million, subject to customary purchase price adjustments as of the closing date (“Purchase Price”).

Helm Bank is a community bank authorized to operate in the State of Florida, United States of America, by the Florida Office of Financial Regulation (“OFR”), regulated by the OFR, and is a member of the Federal Deposit Insurance Corporation (“FDIC”).

The transaction is subject to obtaining the required regulatory approvals in the United States from the OFR and the Federal Reserve (“FED”), and in Peru from the Superintendencia de Banca, Seguros y AFP (“SBS”), as well as the fulfillment of other customary closing conditions. As of the date of this report, such approvals remain pending.

|

3 |

MATERIAL ACCOUNTING POLICIES |

The material accounting policies used in the preparation of Credicorp’s consolidated financial statements are detailed below:

| a) | Basis of presentation, use of estimates and changes in accounting policies – |

The accompanying consolidated financial statements have been prepared in accordance with IFRS Accounting Standards as issued by the International Accounting Standards Board (IASB).

The consolidated financial statements as of December 31, 2025, and 2024, have been prepared following the historical cost criteria, except for investments at fair value through profit or loss, investments at fair value through other comprehensive income, financial assets designated at fair value through profit or loss, derivative financial instruments, and financial liabilities at fair value through profit or loss, which have been measured at fair value.

The consolidated financial statements are presented in Soles (S/), which is the functional currency of Credicorp Ltd and subsidiaries, see paragraph (c) below, and values are rounded to thousands of soles, except when otherwise indicated.

The preparation of the consolidated financial statements in accordance with IFRS Accounting Standards requires Management to make estimates and use assumptions that affect the reported amounts of assets, liabilities, revenues and expenses, as well as the disclosure of significant events in notes to the consolidated financial statements.

Estimates and judgments are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the current circumstances. The final results could differ from said estimates.

The most significant estimates included in the consolidated financial statements relate to the

calculation of the expected credit loss allowance for the loan portfolio, in accordance with IFRS 9; the uncertainty regarding income tax treatments, in accordance with IFRIC 23; and the estimation of the liability for life insurance contracts

under the General Measurement Model, as established in IFRS 17.

Furthermore, other estimates exist, such as: valuation of investments, liabilities for incurred but not reported claims, useful life of intangibles, impairment of goodwill, of the allowance of the expected credit loss on investments at fair value through other comprehensive income and investments at amortized cost, the valuation of derivative financial instruments and deferred income tax. The accounting criteria used for these estimates are described below.

The Group has adopted the following standards and amendments for the first time for its annual period beginning on or after January 1, 2025, as described below:

| (i) | Amendments to IAS 21: Lack of Exchangeability |

The amendments to IAS 21 “The Effects of Changes in Foreign Exchange Rates” specify how an entity should assess whether a currency is exchangeable and how it should determine a spot exchange rate when exchangeability does not exist. The amendments also require the disclosure of information that enables users of the financial statements to understand how the lack of exchangeability affects, or is expected to affect, the entity’s financial performance, financial position, and cash flows.

Management has estimated the exchange rate for the Bolivian subsidiaries by applying the commission established by the regulator to the exchange rate. See Note 30.2(a)(ii).

| b) | Basis of consolidation – |

Investment in subsidiaries -

The consolidated financial statements comprise the financial statements of Credicorp and its Subsidiaries for all the years presented.

In accordance with IFRS 10 “‘Consolidated Financial Statements”, all entities over which the Group has control are subsidiaries. Control is achieved when the Group is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee. The Group controls an investee if, and only if, it has:

| - | Power over the investee (i.e., existing rights that give it the current ability to direct the relevant activities of the investee), |

| - | Exposure, or rights, to variable returns from its involvement with the investee, and |

| - | The ability to use its power over the investee to affect its returns. |

Generally, there is a presumption that a majority of voting rights results in control. To support this presumption and when the Group has less than a majority of the voting rights or similar rights of an investee, the Group considers all relevant facts and circumstances in assessing whether it has power over the investee, including:

| - | The contractual arrangement with the other holders of voting rights over the investee. |

| - | Rights arising from other contractual arrangements. |

| - | The Group’s voting rights and potential voting rights. |

The Group assesses whether or not it controls an investee if the facts and circumstances indicate that there are changes in any of the elements of control. Consolidation of a subsidiary begins when the Group obtains control over the subsidiary and ceases when the Group loses control of the subsidiary. The consolidated financial statements include assets, liabilities, income and expenses of Credicorp and its subsidiaries.

The profit or loss for the period and each component of other comprehensive income are attributed to the owners of the parent and to non-controlling interests, even if this results in non-controlling interests having a negative balance. When necessary, adjustments are made to the financial statements of subsidiaries to align their accounting policies with those of the Group.

All assets and liabilities, equity, income, expenses, and cash flows relating to transactions between members of the Group are fully eliminated on consolidation. Assets held in custody or under management by the Group, such as investment funds, private pension funds (AFP Funds), and others, are not part of the Group’s consolidated financial statements (see Note 3(w)).

Transactions with non-controlling interests -

A change in the ownership interest of a subsidiary, without a loss of control, is accounted for as an equity transaction and any resulting difference between the price paid and the amount by [which] the non-controlling interests are adjusted is recognized directly in the consolidated statement of changes in equity.

The Group does not record any additional goodwill after the purchase of the non-controlling interest, nor does it recognize a gain or loss from the sale of the non-controlling interest.

Loss of control -

If the Group loses control over a subsidiary, it derecognizes the carrying amount of the related assets (including goodwill) and liabilities, non-controlling interest and other components of equity, while any resultant gain or loss is recognized in profit or loss. Any residual investment retained is recognized at fair value.

Investments in associates -

An associate is an entity over which the Group has significant influence. Significant influence is the power to participate in the financial and operating policy decisions of the entity, but without exercising control over said policies.

The Group’s investments in its associates are initially recognized at cost and subsequently accounted for using the equity method. These investments are included in “Other assets” in the consolidated statement of financial position; the results arising from the application of the equity method are included in “Net gain on securities” in the consolidated statement of income.

As of December 31, 2025 and 2024, the following entities comprise the Group (the individual or consolidated figures of their financial statements are presented in accordance with IFRS Accounting Standards and before eliminations for consolidation purposes, except for the elimination of Credicorp’s treasury shares and its related dividends):

| Entity | Activity and country of incorporation | Percentage of interest (direct and indirect) | Assets | Liabilities | Equity | Net profit (loss) | |||||||||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2023 | |||||||||||||||||||||||||

| % | % | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||||||||

| Grupo Crédito S.A. and Subsidiaries (i) | Holding, Peru | 100.00 | 100.00 | 241,448,365 | 231,724,646 | 203,624,697 | 197,418,592 | 37,823,668 | 34,306,054 | 6,475,332 | 5,179,505 | 4,562,831 | |||||||||||||||||||||||

| Pacífico Compañía de Seguros y Reaseguros S.A and Subsidiaries (ii) |

Insurance, Peru | 98.86 | 98.86 | 20,619,872 | 17,890,138 | 16,309,989 | 14,504,765 | 4,309,883 | 3,385,373 | 784,502 | 765,767 | 803,384 | |||||||||||||||||||||||

| Atlantic Security Holding Corporation and Subsidiaries (iii) |

Capital Markets, Cayman Islands | 100.00 | 100.00 | 5,390,195 | 6,014,937 | 4,040,240 | 5,026,510 | 1,349,955 | 988,427 | 737,562 | 569,689 | 474,780 | |||||||||||||||||||||||

| Credicorp Capital Ltd. and Subsidiaries (iv) | Capital Markets and asset management, Bermudas |

100.00 | 100.00 | 6,707,397 | 5,235,733 | 5,395,856 | 4,070,432 | 1,311,541 | 1,165,301 | 100,479 | 58,501 | (135,495 | ) | ||||||||||||||||||||||

| CCR Inc.(v) | Special purpose Entity, Bahamas | 100.00 | 100.00 | 202 | 260 | 1 | 4 | 201 | 256 | (55 | ) | (22 | ) | (106 | ) | ||||||||||||||||||||

| (i) | Grupo Crédito is a company whose main activities are to carry out management and administration activities of the Credicorp Group's subsidiaries and invest in shares listed on the Peruvian Stock Exchange and unlisted shares of Peruvian companies. we present the individual or consolidated figures of their financial statements are presented in accordance with IFRS Accounting Standards and before eliminations for consolidation purposes: |

| Entity | Activity and country of incorporation | Percentage of interest (direct and indirect) | Assets | Liabilities | Equity | Net profit (loss) | |||||||||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2023 | |||||||||||||||||||||||||

| % | % | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||||||||

| Banco de Crédito del Perú and Subsidiaries (a) | Banking, Peru | 97.74 | 97.74 | 219,933,373 | 211,086,260 | 191,487,370 | 184,934,666 | 28,446,003 | 26,151,594 | 6,500,570 | 5,311,804 | 4,583,662 | |||||||||||||||||||||||

| Inversiones Credicorp Bolivia S.A. and Subsidiaries (b) |

Banking, Bolivia | 99.92 | 99.96 | 10,910,443 | 14,028,528 | 10,144,528 | 13,106,538 | 765,915 | 921,990 | 85,379 | 92,781 | 84,898 | |||||||||||||||||||||||

| Prima AFP (c) | Private pension fund administrator, Peru |

100.00 | 100.00 | 684,509 | 657,971 | 231,235 | 182,419 | 453,274 | 475,552 | 146,543 | 132,926 | 149,549 | |||||||||||||||||||||||

| Tenpo SpA and Subsidiaries (d) | Holding, Chile | 100.00 | 100.00 | 2,063,256 | 903,698 | 1,708,824 | 646,952 | 354,432 | 256,746 | (148,391 | ) | (118,344 | ) | (111,692 | ) | ||||||||||||||||||||

| Yape Market (e) | Digital platform for e-commerce | 100.00 | 100.00 | 149,960 | 119,137 | 69,283 | 60,567 | 80,677 | 58,570 | (7,993 | ) | (35,190 | ) | (8,345 | ) | ||||||||||||||||||||

| Krealo Management (f) | Management and development of digital businesses and innovation | 99.99 | 99.99 | 89,338 | 54,414 | 51,766 | 7,175 | 37,572 | 47,239 | (72,029 | ) | (55,679 | ) | – | |||||||||||||||||||||

| Compañía Incubadora de Soluciones Móviles S.A - Culqi (g) | Payment Processing Services | 100.00 | 100.00 | 225,546 | 200,890 | 171,339 | 134,725 | 54,207 | 66,165 | (62,458 | ) | (90,040 | ) | (89,075 | ) | ||||||||||||||||||||

| Other minors Subsidiaries (h) | 3,054 | 2,715 | 1,105 | 570 | 1,949 | 2,145 | (836 | ) | (1,194 | ) | (565 | ) | |||||||||||||||||||||||

| a) | BCP was established in 1889 and its activities are regulated by the Superintendency of Banks, Insurance and Pension Funds -Perú (the authority that regulates banking, insurance and pension funds activities in Perú, hereinafter “the SBS"). |

Its main Subsidiary is Mibanco, Banco de la Microempresa S.A. (hereinafter “Mibanco”), a banking entity in Perú oriented towards the micro and small business sector. As of December 31, 2025, the assets, liabilities, equity and net result of Mibanco amount to approximately S/18,372.4 million, S/15,570.4 million, S/2,802.0 million and S/455.3 million, respectively (S/16,947.3 million, S/14,279.3 million, S/2,668.0 million and S/309.1 million, respectively December 31, 2024).

| b) | Inversiones Credicorp Bolivia S.A. (hereinafter “ICBSA”) was established in February 2013 and its objective is to make capital investments for its own account or for the account of third parties in companies and other entities providing financial services, exercising or determining the management, administration, control and representation thereof, both nationally and abroad, for which it can invest in capital markets, insurance, asset management, pension funds and other related financial and/or stock exchange products. |

Its principal Subsidiary is Banco de Crédito de Bolivia (hereinafter “BCB”), a commercial bank which operates in Bolivia. As of December 31, 2025, the assets, liabilities, equity and net result of BCB were approximately S/10,865.5 million, S/10,046.5 million, S/819.0 million and S/85.9million, respectively (S/13,974.7 million, S/12,968.7 million, S/1,006.0 million and S/93.5 million, respectively as of December 31, 2024).

| c) | Prima AFP is a private pension fund administrator, and its activities are regulated by the SBS. |

| d) | Tenpo SpA (hereinafter “Tenpo", before “Krealo SpA”) was established in Chile in January 2019; and is oriented to make capital investments

outside the country. On July 1, 2019, Tenpo (Krealo SpA) acquired Tenpo Technologies SpA (before “Tenpo SpA”) and Tenpo Prepago S.A. (before “Multicaja Prepago S.A.”). This group of companies offers certain financial products and is

currently undergoing the regulatory approval process before the Chilean Superintendency of Banks and Financial Institutions for the granting of a banking license and the establishment of Tenpo Bank. |

| e) | Yape Market S.A.C. (“Yape Market”) was incorporated on July 1, 2022, and its main activity is to offering promotion, sales management, and product and service placement solutions through a digital commerce platform. |

| f) | Krealo Management S.A. (hereinafter, “Krealo Management”) was incorporated in September 2022 and its objective is to make investments and participate in the equity of other domestic and foreign companies. Its subsidiaries are Wally POS S.A.C., Sami Shop S.A.C., and Monokera S.A.C. |

| g) | Culqi (hereinafter, “Culqi”) was created in December 2013, and its principal activity is to provide digital payment processing services, which consist of collecting consumer payments through online or physical platforms. |

| h) | Other minor subsidiaries include Inversiones 2020 S.A, and Soluciones en Procesamiento S.A. |

| (ii) | Pacífico Seguros is an entity supervised by the SBS, whose economic activities include the underwriting and administration of general and life insurance policies, reinsurance operations, as well as real estate and financial investments. It has subsidiaries including Crediseguro Seguros Personales, Crediseguro Seguros Generales, Pacífico Asiste, and Pacífico EPS and its subsidiaries, which actively participate in the multiple insurance and health insurance businesses, respectively. |

| (iii) | Its most important subsidiary is ASB Bank Corp. (merged with Atlantic Security Bank on August 2021, was established in September 9, 2020 in the Republic of Panama; its main activities are private and institutional banking services and trustee administration, mainly for BCP’s Peruvian customers. |

| (iv) | Credicorp Capital Ltd. was formed in 2012, and its main subsidiaries are Credicorp Capital Holding Peru (owner of Credicorp Capital Perú S.A.A.), Credicorp Holding Colombia (owner of Credicorp Capital Colombia and Mibanco – Banco de la Microempresa de Colombia S.A.), and Credicorp Capital Holding Chile (owner of Credicorp Capital Chile), which carry out their activities in Peru, Colombia and Chile, respectively. We present below the consolidated financial statements in accordance with IFRS and before eliminations for consolidation purposes: |

| Entity | Percentage of interest (direct and indirect) | Assets | Liabilities | Equity | Net profit (loss) | ||||||||||||||||||||||||||||

| 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2025 | 2024 | 2023 | |||||||||||||||||||||||

| % | % | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | S/(000) | |||||||||||||||||||||||

| Credicorp Holding Colombia S.A.S. and Subsidiaries (a) | 100.00 | 100.00 | 5,518,459 | 4,204,281 | 4,591,242 | 3,404,834 | 927,217 | 799,447 | 88,288 | 27,913 | (163,342 | ) | |||||||||||||||||||||

| Credicorp Capital Holding Chile and Subsidiaries (b) | 100.00 | 100.00 | 841,116 | 717,727 | 673,028 | 548,753 | 168,088 | 168,974 | 1,345 | 9,460 | (10,716 | ) | |||||||||||||||||||||

| Credicorp Capital Holding Perú S.A. and Subsidiaries (c) | 100.00 | 100.00 | 293,616 | 278,115 | 124,127 | 111,448 | 169,489 | 166,667 | 21,215 | 21,958 | 4,318 | ||||||||||||||||||||||

| a) | Credicorp Holding Colombia was incorporated in Colombia on March 5, 2012, and its main purpose is the administration, management and increase of its equity through the promotion of industrial and commercial activity, through investment in other companies or legal persons. |

Its main subsidiaries are Credicorp Capital Colombia S.A, which was acquired in Colombia in 2012 and merged with Ultraserfinco S.A. In June 2020, this subsidiary is oriented to the activities of commission agents and securities brokers. Likewise, Mibanco Colombia (before Banco Compartir S.A.) was acquired in 2019 and merged with Edyficar S.A.S. in October 2020, this subsidiary is oriented to grant credits to the micro and small business sector. As of December 31, 2023, Credicorp Holding Colombia has recognized an impairment of the goodwill of Mibanco Colombia for S/64.1 million (Credicorp’s equity holders), see Note 10(b).

As of December 31, 2025, and 2024, the direct and indirect interest held by Credicorp and the assets, liabilities, equity and net income were:

| Entity | Percentage of interest (direct and indirect) | Assets | Liabilities | Equity | Net profit (loss) | ||||||||||||||||||||||||||||